A REVERSE MORTGAGE SAVED A FAMILY FROM LOSING THEIR HOME

In my book Retirement Solutions for Smart People, I describe many situations in which a reverse mortgage helped people who could not qualify for a conventional loan because of limited income or other financial circumstances. In every one of those cases, the goal was the same: to help people enjoy a more secure retirement.

Recently, I encountered a very different situation. The client was someone I had helped twice before, in 2001 and again in 2007. At that time, despite her limited income, I was able to find financing that met her needs. Today, her circumstances have changed dramatically. She is suffering from a serious disease and can no longer care for herself.

A few weeks ago, I received a call from her daughter, whom I had known for many years. She explained that her mother had two existing mortgages and that the payments had fallen behind. The home was already in pre-foreclosure. The situation was heartbreaking.

The house had accumulated substantial equity over the years. Four family members, including the mother, were living there. Selling the home was not the daughter’s first choice because she understood that, after her mother’s passing, the property would receive a step-up in tax basis, potentially eliminating a large capital gains tax. What the family needed most was time.

Unfortunately, there were many obstacles.

The mortgages were in the mother’s name. Because of not making mortgage payments, her credit score was only 570 and her income was just $900 a month from Social Security. Under conventional lending guidelines, there was virtually no chance of obtaining a new loan.

Fortunately, there was another solution.

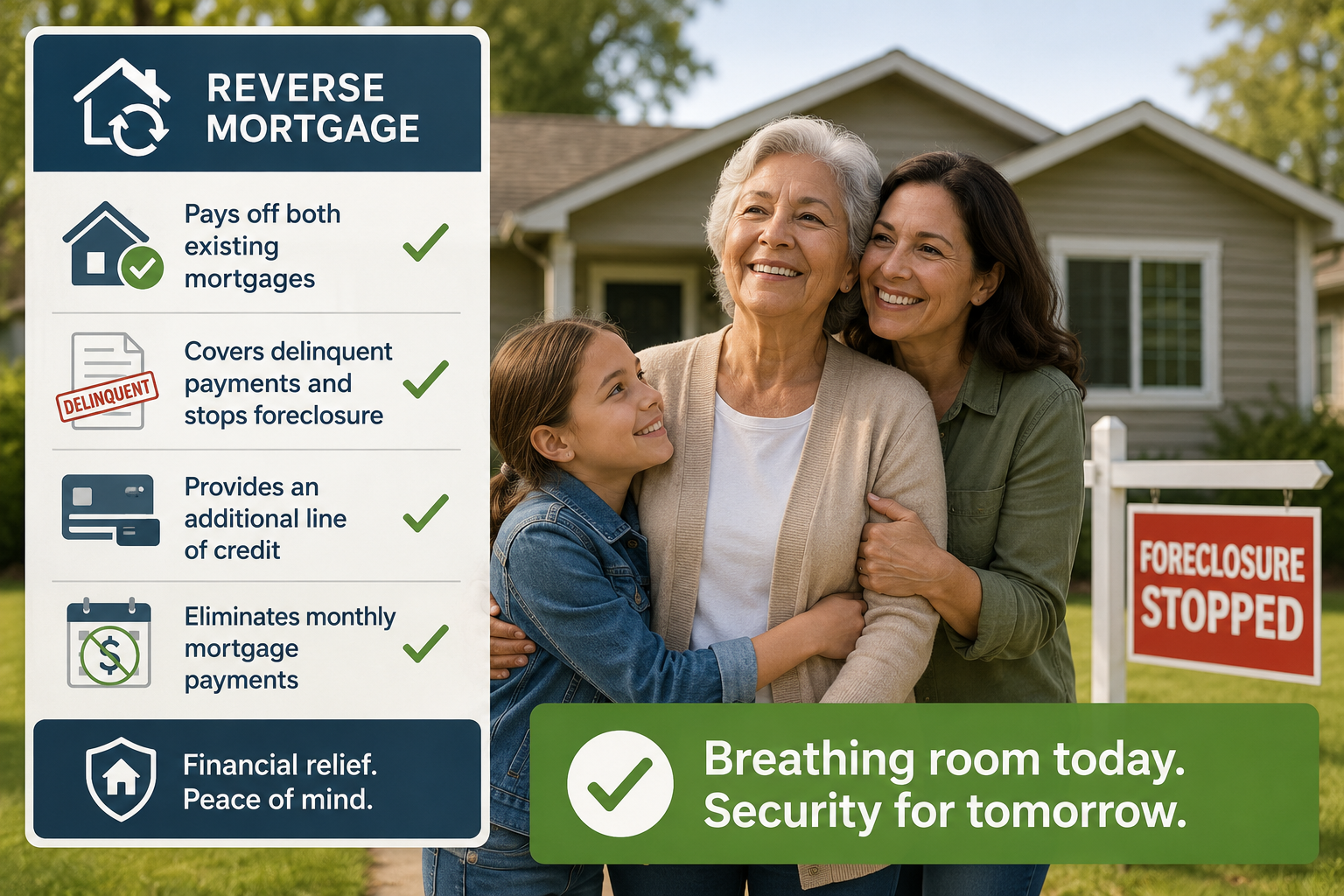

Because the mother was over 62 and owned a home with significant equity, she qualified for a reverse mortgage. The reverse mortgage would pay off both existing mortgages, covered the delinquent payments that had placed the home in foreclosure, and provided an additional line of credit for future needs. Most importantly, it would eliminate the monthly mortgage payments giving the family the breathing room they desperately needed.

Even after more than four decades in the mortgage business, this case reminded me that every family’s circumstances are unique. Sometimes the solution is not obvious, but it does exist. Many homeowners believe they have run out of options simply because their income is too low or their financial situation appears impossible. If they have built equity in their home, there may be a solution they have never considered.

That is why I always encourage people not to wait until the last moment.

If you or someone you know is struggling with mortgage payments but has substantial equity in a home or condominium, give me a call. Together, we can determine whether a reverse mortgage—or another financing strategy—can provide the financial relief you need.

You may be surprised to discover that there is still a way forward.

Meanwhile please order on Amazon one of my books I wrote on the subject — Retirement Solutions for Smart People, which is also available on Kindle. And while you are there, you can also buy Reflection. The Healing Images.

I am grateful in advance.

Manny Kagan,

Your professional mortgage broker since 1983

(415) 225-7920; mannykagan@comcast.net