THREE REVERSE MORTGAGE CALLS FROM ICELAND

While on vacation in Iceland, I still found time to work for a few hours each day. Because Iceland is seven hours ahead of California, I was able to handle business between 4:00 p.m. and 6:00 p.m., before heading to dinner.

During those two hours, I spoke with existing clients, a new client, and received several calls. Three of those calls involved reverse mortgages, and each demonstrated how this financial tool can help people facing very different life situations.

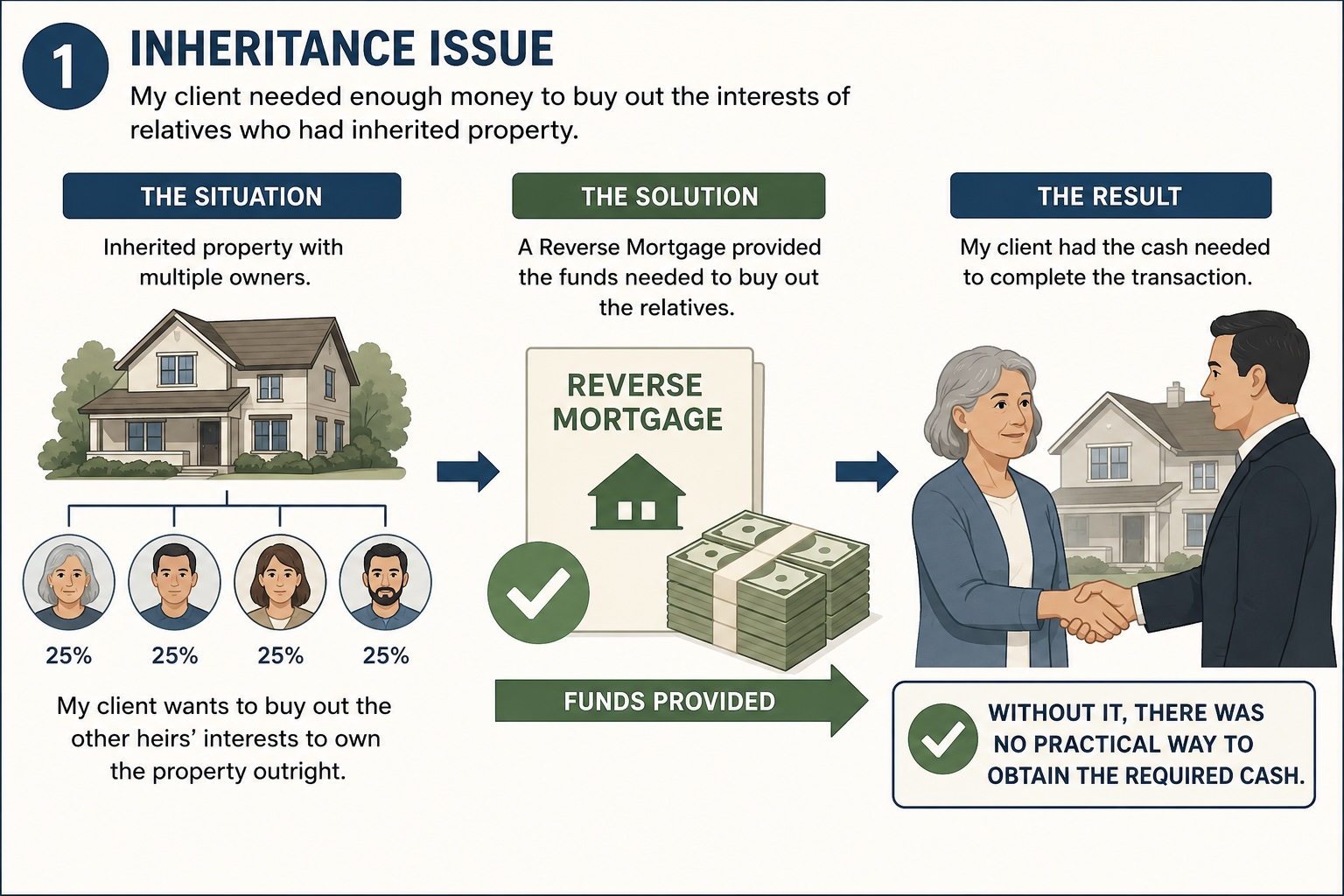

The first call involved an inheritance issue. My client needed enough money to buy out the interests of relatives who had inherited property. A reverse mortgage provided the funds needed to complete the transaction. Without it, there was no practical way to obtain the required cash.

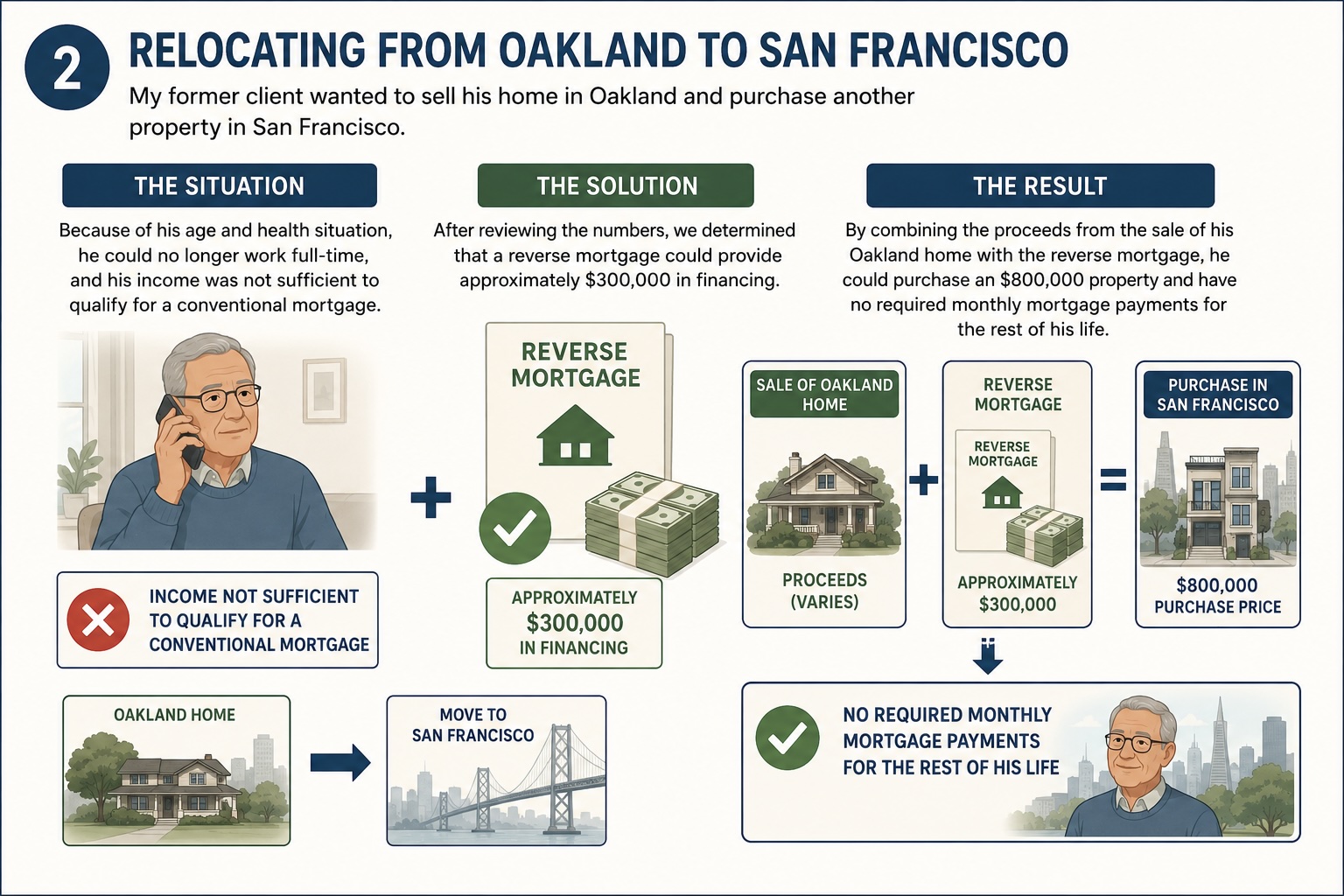

The second call came from a former client who wanted to sell his home in Oakland and purchase another property in San Francisco. Because of his age and health situation, he could no longer work full-time, and his income was not sufficient to qualify for a conventional mortgage. After reviewing the numbers, we determined that a reverse mortgage could provide approximately $300,000 in financing. By combining the proceeds from the sale of his Oakland home with the reverse mortgage, he could purchase an $800,000 property and have no required monthly mortgage payments for the rest of his life.

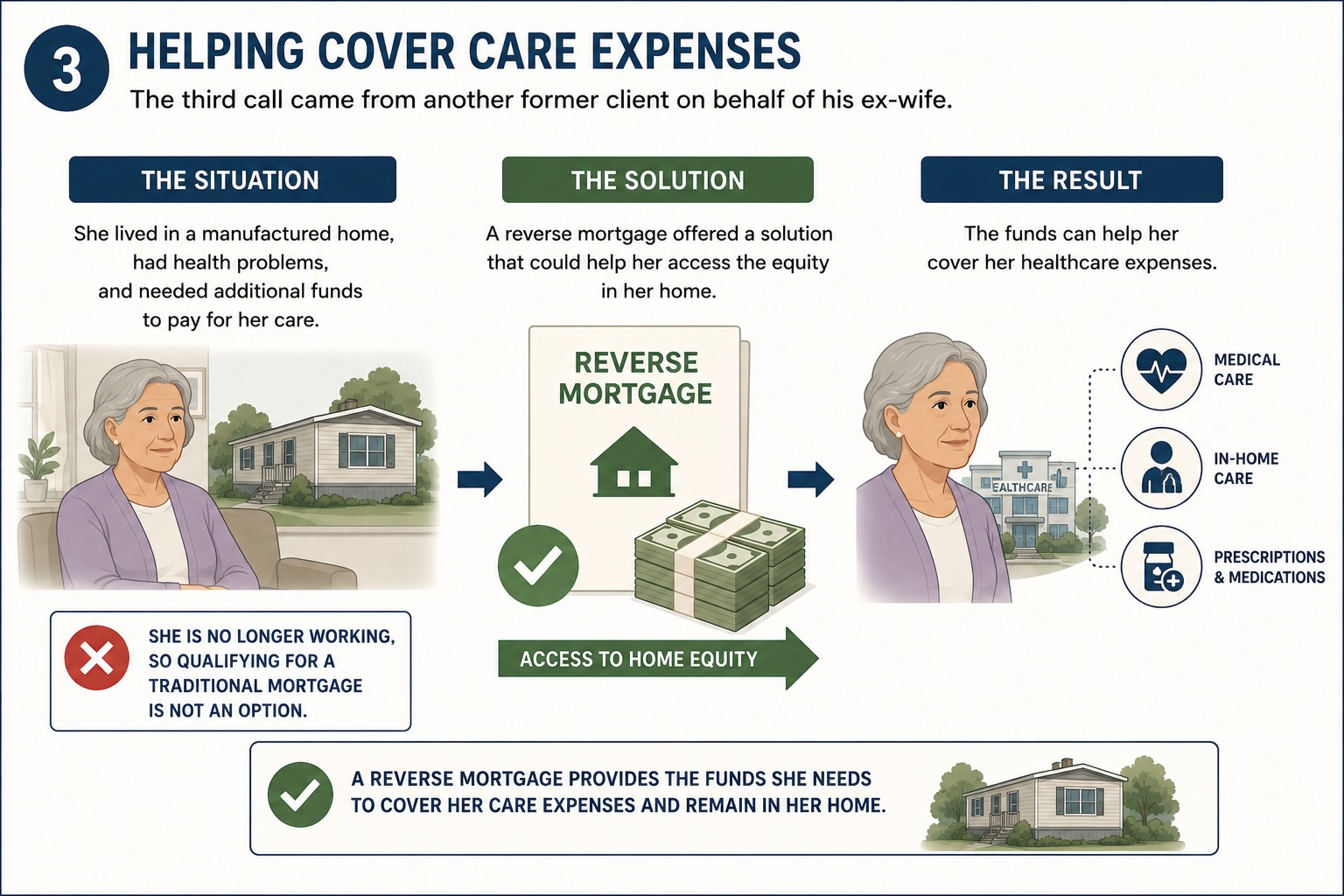

The third call came from another former client on behalf of his ex-wife. She lived in a manufactured home, had health problems, and needed additional funds to pay for her care. Since she was no longer working, qualifying for a traditional mortgage was not an option. A reverse mortgage offered a solution that could help her access the equity in her home and cover her healthcare expenses.

These were three completely different situations, yet in each case a reverse mortgage provided a practical solution. One lesson I have learned over the years is that it is often better to prepare before a financial need arises. Establishing a reverse mortgage line of credit while you qualify can provide a valuable source of funds later in life. If obtaining a conventional line of credit becomes difficult because of retirement or reduced income, your home equity may still be available to help meet future needs.

If you have questions about reverse mortgages or would like to discuss whether one might be appropriate for your situation, please give me a call.

Manny Kagan

(415) 225-7920