ADDING A LINE OF CREDIT BEHIND YOUR FIRST MORTGAGE: HOW IT WORKS

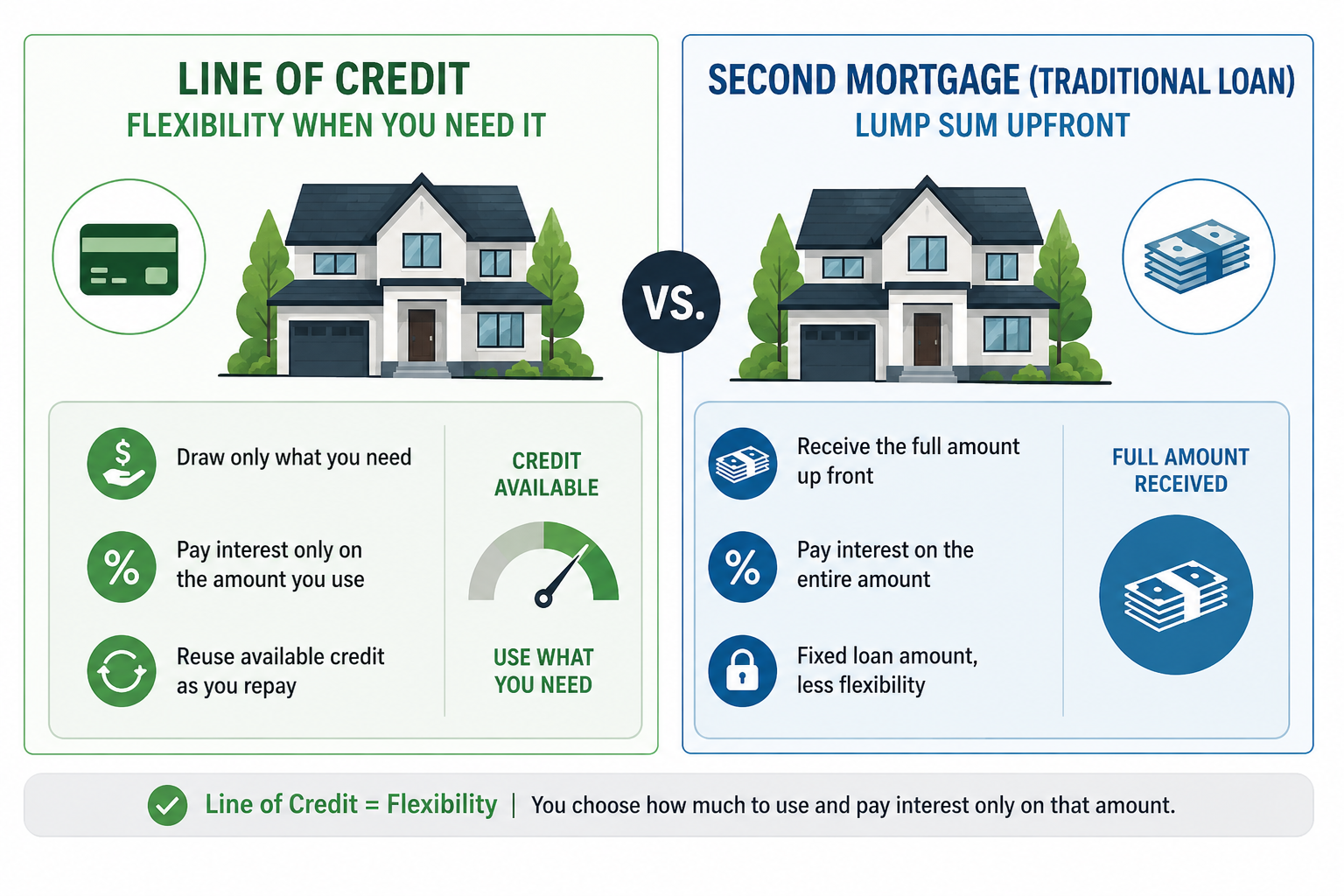

Sometimes I get calls from clients who need a line of credit behind their first mortgage. Instead of taking a traditional second loan, many clients prefer a line of credit because it offers flexibility. You can draw only the amount you need and pay interest only on that amount, unlike a second mortgage where you receive the full amount at once.

Recently, we had a presentation in our office by Suzie De Leon from Angel Oak Lending. She introduced an interesting option for qualifying for a line of credit using bank statements instead of traditional income documentation.

One advantage of this program is that borrowers may not need to show large taxable income to qualify. By using bank statements to calculate income, some self-employed borrowers and business owners may have more opportunities to qualify for a combination of a first mortgage and a line of credit.

This type of financing can sometimes be easier to obtain if you have enough equity in your property. However, it is important to understand that payments may be higher because of the way these programs are structured.

If you need any type of mortgage loan, including a line of credit, give me a call — I may be able to help.

Thank you,

Manny Kagan,

Your professional mortgage broker since 1983

(415) 225-7920; mannykagan@comcast.net