EVERY CLIENT HAS THEIR OWN

UNIQUE SOLUTION

A few days ago, I received a very interesting phone call from a real estate agent I’ve known for many, many years. He opened with a simple question: “Do you do DSCR loans?” That immediately caught my attention—because we do all types of loans. So, I asked him a few more questions to understand the situation. It turns out he was thinking about buying a four-unit property for his daughter. In his mind, a DSCR loan was the solution. But as we dug deeper, the picture changed.

His daughter is employed, has income, and can actually qualify for a traditional loan, and intends to live in one of the units. In this case, she could potentially purchase the property with as little as 10% down—and likely get better terms than a DSCR loan.

So, here’s the key point: Not every situation requires a DSCR loan—sometimes a conventional approach is the better solution.

Now, DSCR loans absolutely have their place. For example, I have a client who recently inherited a property from his mother and is buying out his brother. In that case, a DSCR loan makes perfect sense—because qualification is based on the income generated by the property, not personal income.

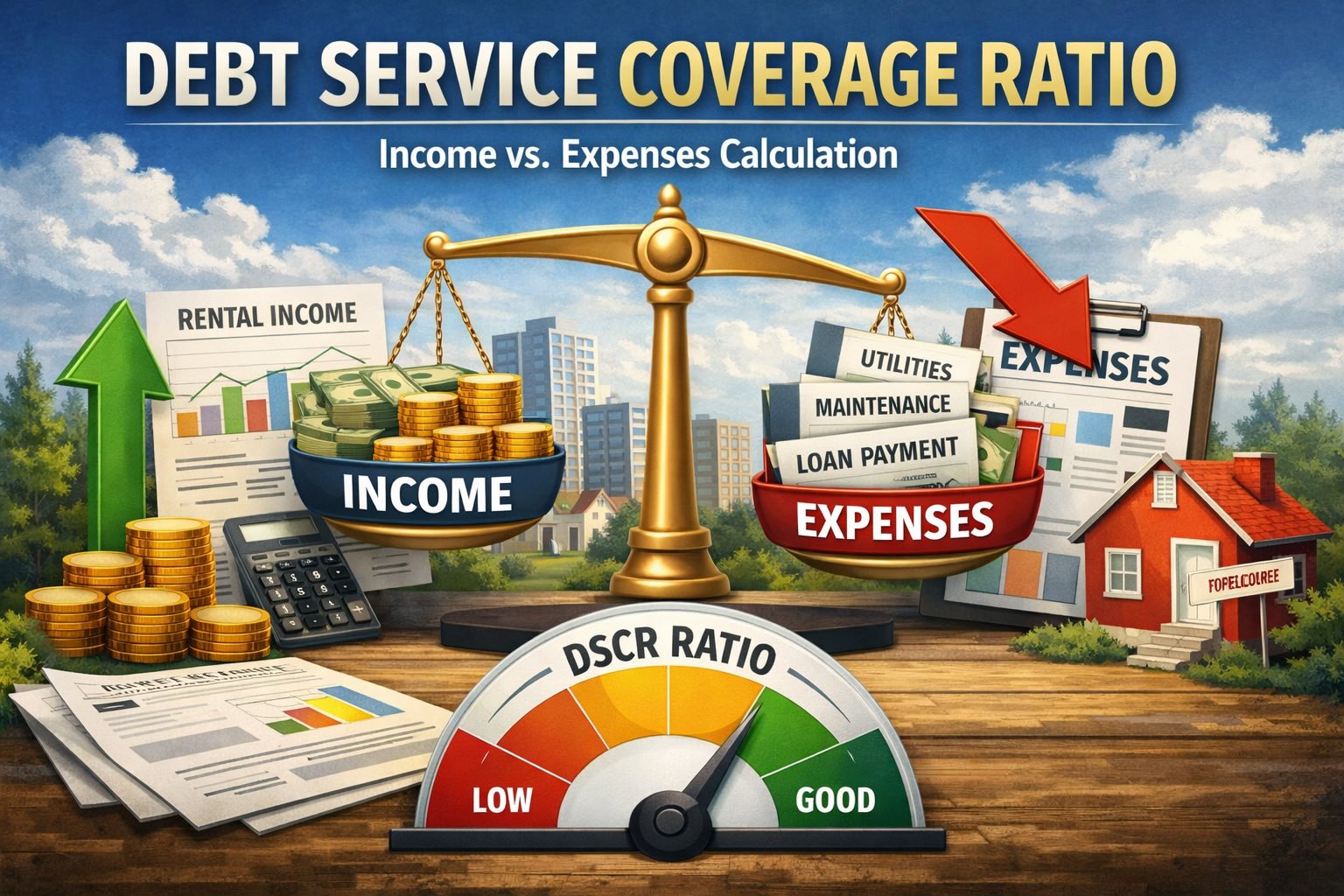

That’s what DSCR stands for: Debt Service Coverage Ratio—a calculation based on the property’s income versus its expenses. And there are different ways to structure it depending on the scenario. So, the lesson is simple: Every situation has a solution—but the right solution depends on understanding the full picture.

One of my lenders shared this flyer with me as an illustration of my expertise. In other words, if you ever have questions, call me. I promise — I’ll help you find the right answer.

Warm regards,

Manny Kagan,

President,

Pacific Bay Financial Corporation

Your professional mortgage broker since 1983