REVISITING THE TOPIC

Not too long ago, I touched on this important question in my social media posts, and I’d like to dive a little deeper today. Many of my clients have been able to buy properties even with very little money for a down payment—and I want to share some insights that could help you too.

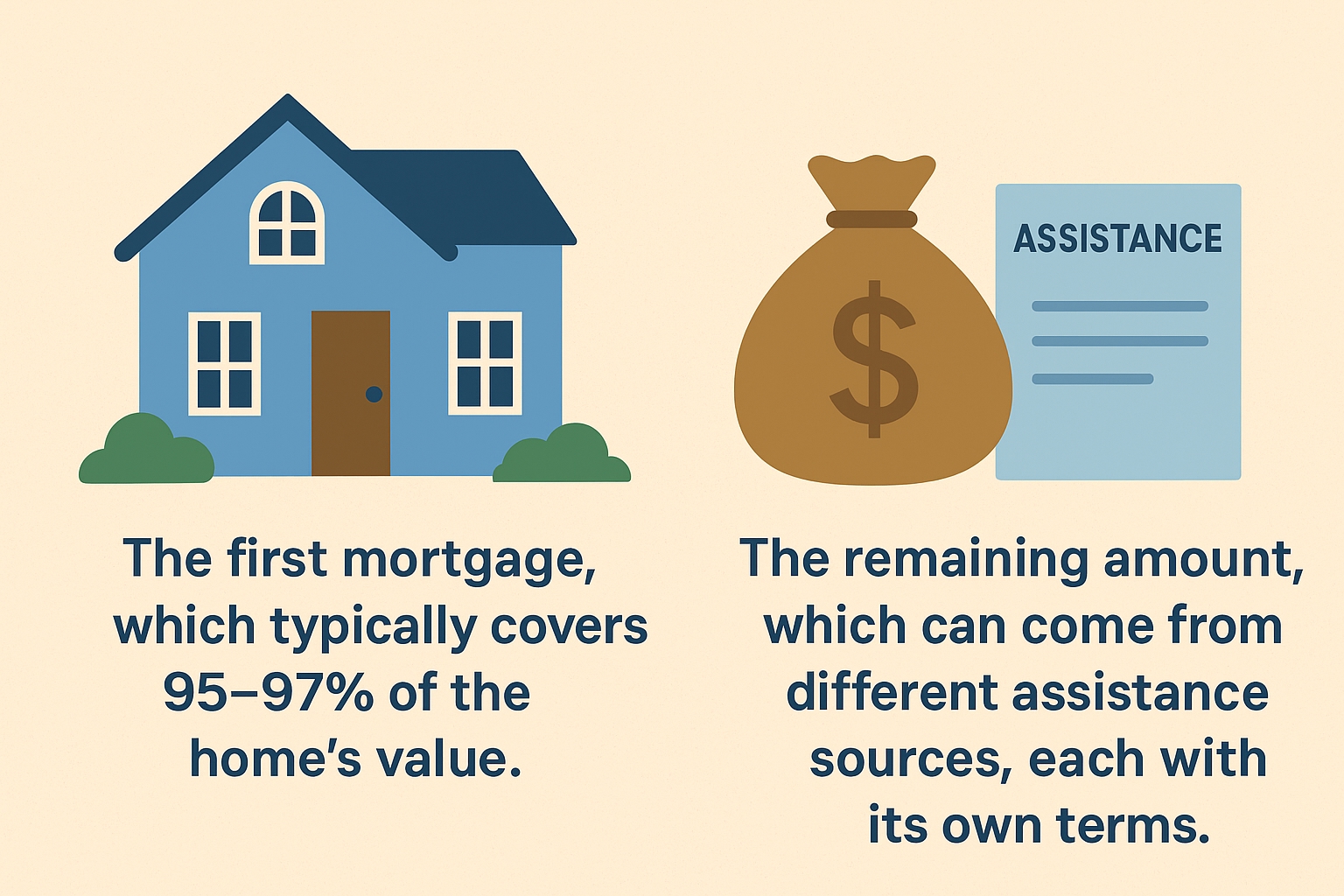

That is possible thanks to a variety of down payment assistance programs available on the market. These programs usually consist of two parts:

- The first mortgage, which typically covers 95–97% of the home’s value.

- The remaining amount, which can come from different assistance sources, each with its own terms.

However, there’s a trade-off: because of the assistance, the interest rate on the first mortgage is often higher. This means a higher required income to qualify. In addition, many of these programs have income limits that can affect eligibility.

Recently, during a recent presentation at our office, Lynn Jackson from Plaza Mortgage discussed how FHA loans can offer 100% financing. Click this link to see a piece of Lynn’s presentation. While that sounds appealing, these loans also come with higher mortgage insurance premiums.

That’s why I often suggest another option: using a gift for the down payment. With as little as 5% down, buyers can qualify for first-time homebuyer programs that often carry lower interest rates compared to down payment assistance loans.

And here’s the key: interest rates are expected to come down. When that happens, we’ll likely see another buying frenzy.

Don’t wait—call me today, and let’s structure your transaction the smart way.

Best wishes,

Manny Kagan,

President,

Pacific Bay Financial Corporation

Your professional mortgage broker since 1983

(415) 225-7920

NMLS #205637

DRE #00874630