THE BENEFITS OF

TENANCY-IN-COMMON FINANCING

Tenancy in Common (TIC) financing has become popular over the years because it can offer buyers opportunities that are sometimes difficult to find with traditional condominiums.

One of the main advantages is price. In many cases, a TIC unit can be purchased for $100,000 or more below the price of a comparable condominium. In some situations, if the building is later converted into condominiums, individual units may sell for significantly higher values.

Another benefit is that many TIC properties are located in older buildings with unique architecture, charm, and desirable locations that newer condominium developments may not offer.

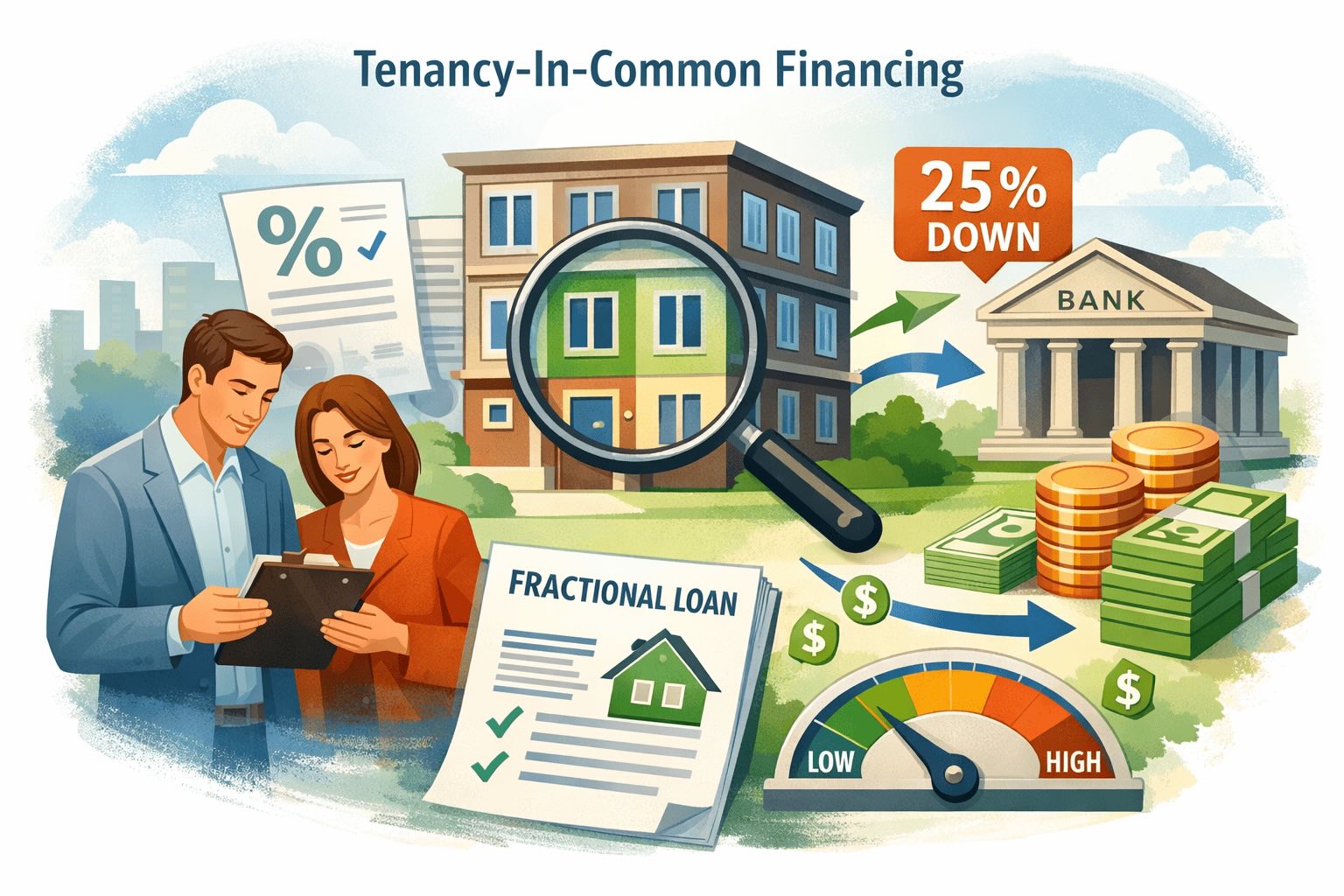

When clients ask me about purchasing a TIC unit, I never discourage them. However, I always recommend comparing it with condominiums as well, because financing for TIC properties is different.

TIC mortgages are usually offered by specialty lenders who provide what is called a fractional loan, meaning the loan is secured by your specific unit rather than the entire building. Because of this structure, loan terms can differ from traditional mortgages.

For example, in one of the banks, their program typically requires around 25% down payment with interest rate which depends partly on the borrower’s banking relationship and deposits with the institution.

One of our lenders offers financing up to 85% loan-to-value, allowing buyers to purchase with as little as 15% down, although the interest rate may be higher. With 20% down, terms are usually more favorable, and loan amounts may go up to $2.5 million. There is no need to keep the money in this particular bank.

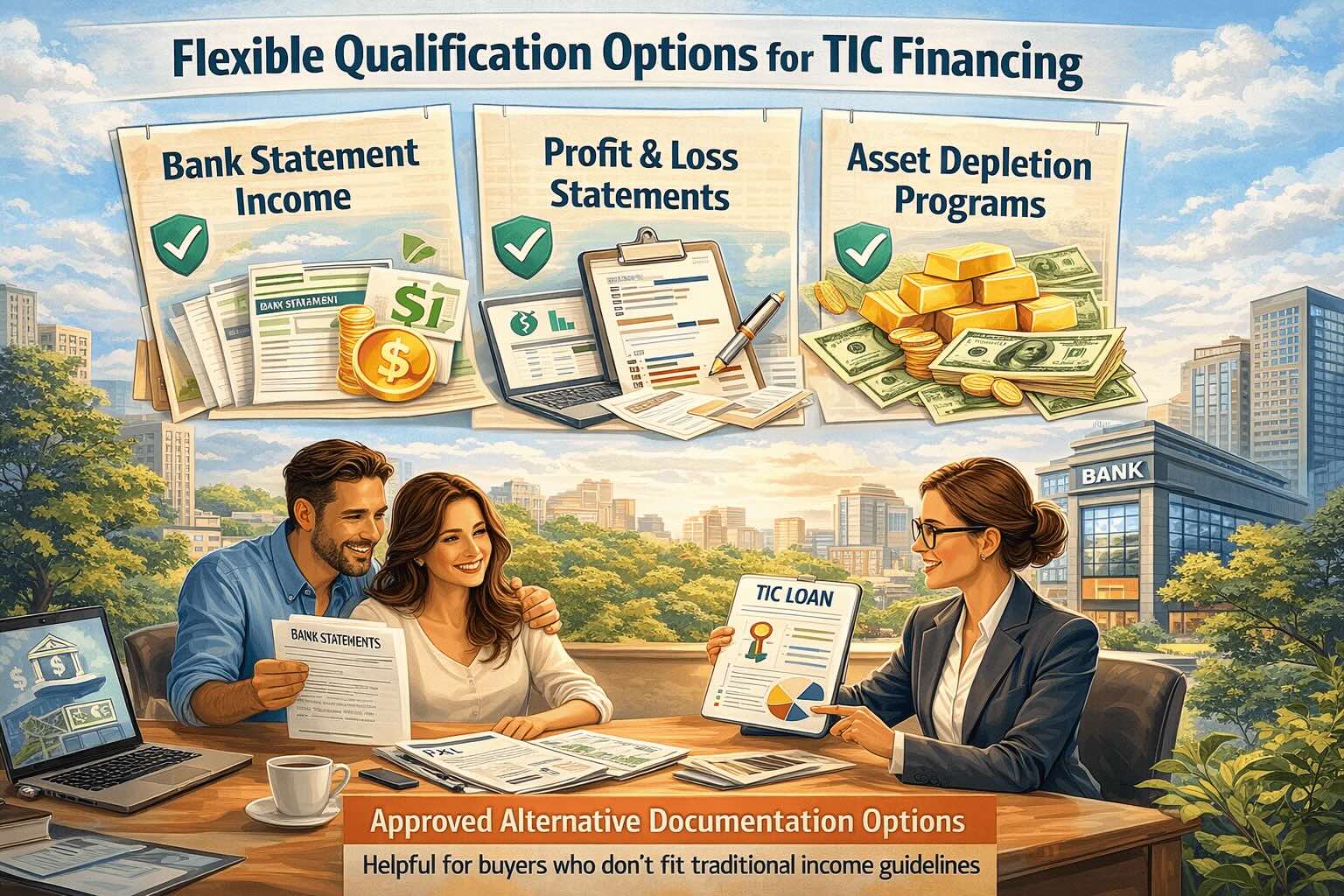

If the client doesn’t have sufficient income to qualify for the loan mortgage, some of these programs also offer flexible qualification options, including:

- bank statement income

- profit and loss statements

- asset depletion programs

These alternatives can be very helpful for buyers who do not fit traditional income documentation guidelines.

If you are considering purchasing a property under a Tenancy in Common (TIC) structure or simply want to explore your options, feel free to contact me. I would be happy to help guide you toward the best financing strategy. Meanwhile, click this link to view my weekly YouTube video.

Warm regards,

Manny Kagan,

President,

Pacific Bay Financial Corporation

Your professional mortgage broker since 1983